Technology

The concept of Blockchain Technology in Simple and easy to comprehend Words.

W

Written by G. Ram Charan

Mar 4, 2026 12 min read

Over the last decade, the term blockchain has become one of the most discussed topics in technology. Many people first heard about it through digital currencies like Bitcoin, but blockchain technology goes far beyond cryptocurrency. Today, companies, governments, and researchers are looking into how blockchain can improve data storage, sharing, and protection.

But what exactly is blockchain? Why do so many experts believe it could change how the internet works? And is it necessary?

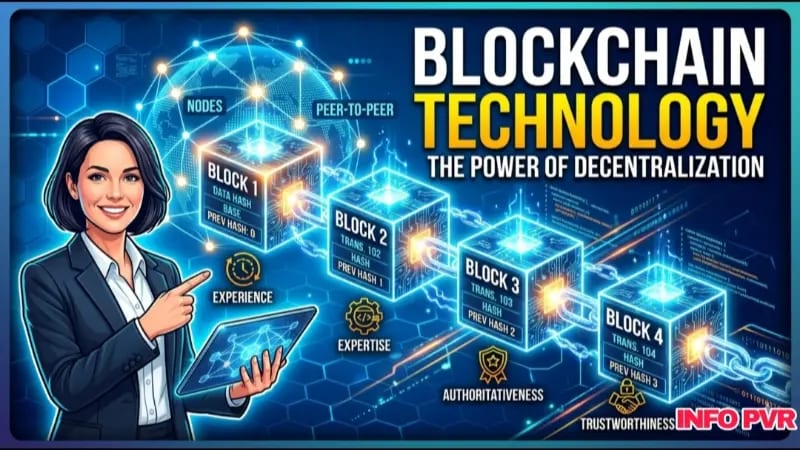

What Is Blockchain?

In simple terms, blockchain is a digital record system that stores information securely and transparently.

Imagine a notebook that keeps track of transactions. Each time something occurs, a new entry is made in the notebook. Now picture that instead of one person holding the notebook, thousands of people around the world have identical copies of it. When a new entry is added, all copies update at once.

That shared notebook is similar to how blockchain functions.

Information is stored in blocks, and each block connects to the previous one. These connected blocks form a chain, which is why its called blockchain. Once a block of information is recorded, it becomes very hard to change or delete it.

This structure makes blockchain extremely secure and reliable.

How Blockchain Works

To understand blockchain, it helps to break the process down into a few simple steps.

First, a transaction or piece of information is created. This could be anything from sending digital currency to recording data about a shipment.

Next, that information is grouped with other transactions into a block.

Then, computers in the network check whether the transaction is valid. This process is known as verification.

Once verified, the block is added to the chain of previous blocks. The updated record is shared with every participant in the network.

Because the information is stored across many computers instead of one central server, the system is called decentralized.

Why Blockchain Is Considered Secure

Security is one of the main reasons blockchain has gained so much attention.

In traditional systems, data is usually stored in a single database controlled by one organization. If someone hacks that database, they can change or steal the information.

Blockchain operates differently. Since copies of the data exist across many computers, altering the record would require changing every copy at the same time, which is incredibly difficult.

Each block also contains a unique digital fingerprint known as a cryptographic hash. If someone tries to change information in a block, the fingerprint changes too, immediately showing that something is wrong.

This combination of decentralization and cryptography makes blockchain highly resistant to fraud and tampering.

Blockchain and Cryptocurrency

Blockchain became widely known due to cryptocurrencies. The first and most famous example is Bitcoin, which was introduced in 2009 by a person or group using the name Satoshi Nakamoto.

Bitcoin uses blockchain as a public ledger that records every transaction ever made. Instead of a bank verifying payments, the blockchain network confirms and records them.

Another well-known platform is Ethereum, which expanded the idea of blockchain by introducing smart contracts. Smart contracts are programs stored on the blockchain that automatically execute when certain conditions are met.

These innovations opened the door for many new uses beyond digital currency.

Real-World Uses of Blockchain

Although cryptocurrency brought blockchain into the spotlight, the technology has potential in many other fields.

Supply Chain Management

Companies are using blockchain to track products as they move through the chain. By recording each stepfrom manufacturing to deliverybusinesses can verify product authenticity and reduce fraud.

Financial Services

Banks and financial institutions are exploring blockchain to make international payments faster and cheaper. Traditional cross-border transactions can take several days, while blockchain systems may complete them in minutes.

Healthcare

Hospitals and healthcare providers can use blockchain to store medical records securely. Patients could control who accesses their data, improving privacy while still allowing doctors to access important information.

Digital Identity

Blockchain may also help create secure digital identity systems. Instead of repeatedly sharing personal documents with different organizations, individuals could use a blockchain-based identity that verifies their information safely.

Advantages of Blockchain Technology

Several reasons make businesses and governments interested in blockchain.

Transparency is one of the biggest advantages. Because all participants can see the same record, its easier to track transactions and reduce disputes.

Another benefit is security. The decentralized structure and cryptographic protection make the system hard to manipulate.

Blockchain also reduces the need for middlemen. In many traditional systems, intermediaries like banks or clearinghouses are needed to verify transactions. Blockchain can automatically perform these tasks through network consensus.

Finally, blockchain can improve efficiency by automating processes and cutting down on paperwork.

Challenges and Limitations

Despite its promise, blockchain technology is not without issues.

One major challenge is scalability. Some blockchain networks struggle to process a high volume of transactions quickly.

Another concern is energy consumption, particularly in systems that rely on heavy computational work to verify transactions.

There is also uncertainty around regulation, as governments globally are still figuring out how to manage blockchain-based services and cryptocurrencies.

Since the technology is still developing, many experts believe it will take time before blockchain is widely used in everyday systems.

The Future of Blockchain

Even with its challenges, blockchain continues to draw interest from technology companies, startups, and governments. Major organizations are investing in research to explore how blockchain can enhance transparency, security, and efficiency across various industries.

Some analysts believe blockchain could play a role in the future of finance, digital identity, and even internet infrastructure. While it may not replace all traditional systems, it has the potential to change how information and transactions are managed online.

Disadvantages of Blockchain Technology.

Although the technology of the blockchain is new and practical in numerous aspects, it does not lack limitations and difficulties. It is knowledge of these drawbacks that makes people observe both sides of the technology.

High Energy Consumption

The energy consumption of blockchain systems is among the primary issues associated with the given technology. Certain blockchain systems are very energy-intensive and demand extensive computational resources to authenticate and transact business. Since a large number of computers are used to keep the network running, this may become electricity consuming. This has posed environmental concerns in most regions across the globe.

Slow Transaction Speed

The use of blockchain transactions can be slower than the conventional digital payment systems at times. This would be more time consuming since all the transactions have to be authenticated by numerous computers across the network. This may cause delays when dealing with a big number of transactions in the system.

Difficult to Modify Data

A very important aspect of block chain is the fact that information is not easy to be manipulated when it has already been recorded. Although this enhances security there is a potential of causing problems with the introduction of wrong data into the system. After the information has been stored, it is not always easy to correct the mistakes.

High Implementation Cost

Organizations may find it costly to establish blockchain systems. Specialized hardware, software, and expert professionals will be required by businesses to construct and operate blockchain networks. The implementation cost can be the issue with small companies.

Absence of Knowledge and Enlightenment.

Blockchain is a technology that is not well comprehended by many. Since it is a recent and complicated phenomenon, it is possible that it cannot be easily adopted by businesses and individuals. Blockchain has to be more commonly used after further education and awareness.

Legal and Regulatory Issues

Some nations have ambiguous rules concerning blockchain technology. The governments continue learning how to interface and control the blockchain-based systems. This ambiguity may hinder the process of adopting the blockchain technology.

Application Security risks.

Even though blockchain can be regarded as a safe technology, the applications developed on its basis can still be vulnerable. The users may be threatened by poorly developed software or by security malpractices.